During a client’s accumulation phase, an investor can usually withstand and maneuver stock markets’ ebbs and flows. But at retirement, a new challenge begins as their planning resets. As clients retire with their pool of accumulated retirement assets, the distribution phase starts, and the biggest obstacle to success often depends on how the markets perform.

If clients happen to retire in a stable or up market, they can usually retire successfully even with limited planning. However, if clients retire in a down market, without proper planning and the help of a financial advisor they can face multiple issues, including sequence of returns risk during the early years of retirement which can erode retirement savings and potentially force a retiree back into the workforce.

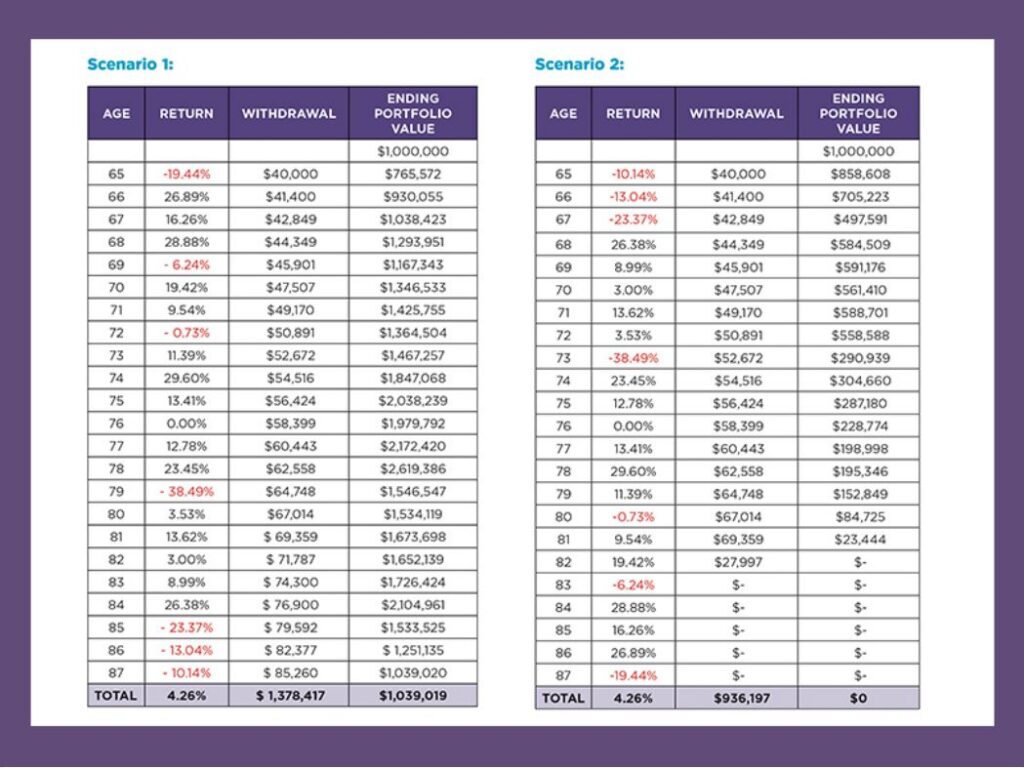

We’ve run some actual numbers to illustrate how this works.

Sequence of Returns Is All About Timing,

But You Can’t Time the Market

Both Scenario 1 and Scenario 2 charts below show actual S&P 500 Index stock returns from 2000 through 2022—except Scenario 1 is in the exact reverse order to what actually took place.

In both scenarios, the ending portfolio value is based on a retiree who retires at 65 with $1 million and withdraws 4% per year plus a 3.5% annual increase for inflation each year through age 87. In Scenario 2, the actual S&P 500 Index, our retiree would have run out of money at age 82.

Life Insurance + Annuity

To Help Avoid Market Risk

Our Scenario 2 hypothetical 65-year-old retiree who stared out with $1 million but experienced market downturns early in retirement could have avoided running out of money by using a guaranteed income fixed indexed annuity (FIA) and cash value life insurance, with contractual policy guarantees provided by the financial strength of the issuing insurance companies.

*By age 87, they could have:

Total portfolio and life insurance cash value: $2,261,726

Total benefit of ownership at 87: $3,640,143

Total legacy: $2,363,027, of which $1,680,193 is tax-free

*These scenarios are based on a prior case; they are hypothetical and for informational purposes only. They are not guarantees. Actual policy values, premiums, benefits, and performance may vary based on underwriting, product selection, client’s age, and carrier requirements. See the whitepaper for more information about this strategy, and contact us for an actual case design for your client.

Learn More About This Strategy By Downloading This Whitepaper:

And call us at 800.440.1088 for a complimentary case design for your client!

Kim is life/health licensed and has worked in the life insurance industry since 1995. Kim spent 16 years at Northwestern Mutual and New York Life working her way from a field assistant to office manager. Because of her extensive experience, she brings a wealth of skills to Quantum. She has acquired the ability to analyze complex alternatives to meet client needs, find efficiencies in application processing, fulfill stringent insurance carrier compliance, and has built strong relationships with numerous carriers top underwriters. Learn More