* UPDATED: As of January 1, 2020, the age at which you must start taking Required Minimum Distributions has changed from 70-1/2 to 72.

As more and more people turn 65 in America, they are learning about the different financial issues they will face in retirement. For instance, take RMDs.

Starting at age 72,* retired people with tax-deferred accounts like 401(k)s are required by the IRS to start withdrawing money, whether they need the income or not.

Some of the accounts with IRS-mandated RMDs include:

- Most 401(k) and 403(b) plans

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- Most tax-deferred retirement accounts

This still surprises many people who may have thought they would spend their retirement in a “lower bracket,” but suddenly find themselves owing the IRS because ordinary income taxes are due on this withdrawn money—every single year.

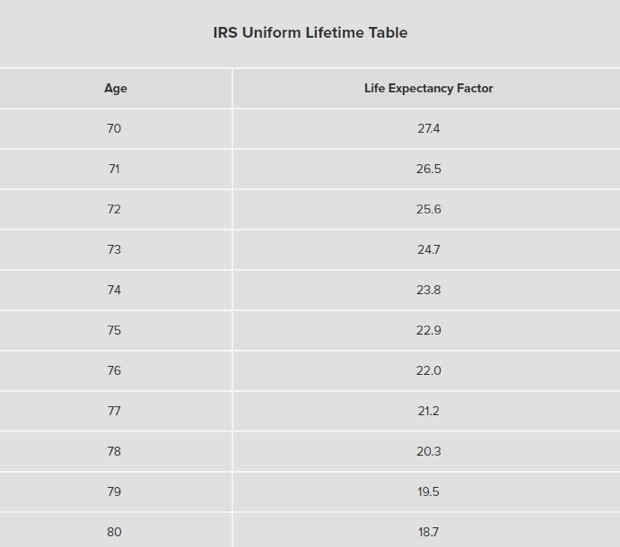

There are precise formulas for calculating how much you have to withdraw each year based on the IRS Uniform Lifetime Table. If you miscalculate, or if you or your plan administrator fail to move the money by midnight on December 31st each year, you could face a 50% tax penalty—and there is no grace period to April 15.

So how exactly do RMDs work?

Let’s start with an extremely simplistic example. Here is a screenshot of part of the IRS’ current factors used to calculate RMDs.

(The table goes up to age 115 and beyond. You can find the IRS life expectancy table as well as an IRS worksheet for calculating RMDs HERE. NOTE: This may change in 2021.)

The math works like this:

Let’s say Joe is single, age 72, has one qualified retirement account and $400,000 was the value of his 401(k) plan as of December 31 of the prior year. Divide $400,000 by Joe’s life expectancy factor of 25.6 from the table, and you get $15,625, which must be withdrawn by Joe by midnight of 12/31.

(NOTE: Joe can withdraw more than that if he wants to.)

The amount withdrawn gets added to Joe’s AGI—adjusted gross income—for the tax year that he is age 72.

As an apples-to-apples comparison, if Joe was 73 and had a $400,000 balance in his 401(k) at the end of the year, he would have had to withdraw $16,194.33 by midnight of 12/31.

In other words, each year as you get older and your life expectancy decreases, the IRS wants you to take out more of your money.

Other Facts You Should Know About RMDs

One of the common questions people ask when they own multiple tax-deferred accounts is which accounts require RMDs, and “can they withdraw from just one account.”

The answer varies based on the types of accounts you own. From the IRS:

An IRA owner must calculate the RMD separately for each IRA that he or she owns, but can withdraw the total amount from one or more of the IRAs. Similarly, a 403(b) contract owner must calculate the RMD separately for each 403(b) contract that he or she owns, but can take the total amount from one or more of the 403(b) contracts.

However, RMDs required from other types of retirement plans, such as 401(k) and 457(b) plans have to be taken separately from each of those plan accounts.

In conclusion:

- HAPPY NEW YEAR, make sure you take your RMDs every year by midnight of December 31.

- Work in conjunction with your financial advisor and CPA or tax professional to help you consider RMDs, taxes and ways to minimize them as part of your overall retirement plan.

- If you’re a financial advisor, call me.

Let’s discuss some strategies that may help your clients with tax-advantaged RMD strategies you might not be aware of, such as indexed universal life insurance. Call Quantum at 800.440.1088 and ask for Jeremy Rogers.

The information in this article is provided for general information and educational purposes only. It is not designed nor intended to be applicable to any person’s individual circumstances. It should not be considered investment advice, nor does it constitute a recommendation that anyone engage in or refrain from a particular course of action.

Do not rely on this information for tax advice. Check with your CPA, attorney or qualified tax advisor for precise information about your specific situation.

Sources:

https://www.kitces.com/blog/irs-proposes-new-rmd-life-expectancy-tables-to-begin-in-2021/

https://www.irs.gov/pub/irs-tege/uniform_rmd_wksht.pdf

https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-required-minimum-distributions

https://www.themoneyalert.com/rmd-tables/

Jeremy has more than 15 years of experience in both the RIA and broker-dealer space. He has worked as a financial advisor, and he holds bachelor’s degrees in both business and economics. Learn More