Below is a potential life strategy that may work for some clients. It may or may not be applicable to your client’s situation, and we recommend that you work in conjunction with your client’s tax professional as well as their tax and/or estate attorney before implementing any specific recommendations related to the client’s personal tax and estate situation. Additionally, the premium rates used in this example are estimates and may vary based on a person’s unique circumstances. Please contact us for a more accurate case design for your clients.

Mr. Johnson, Business Owner Client

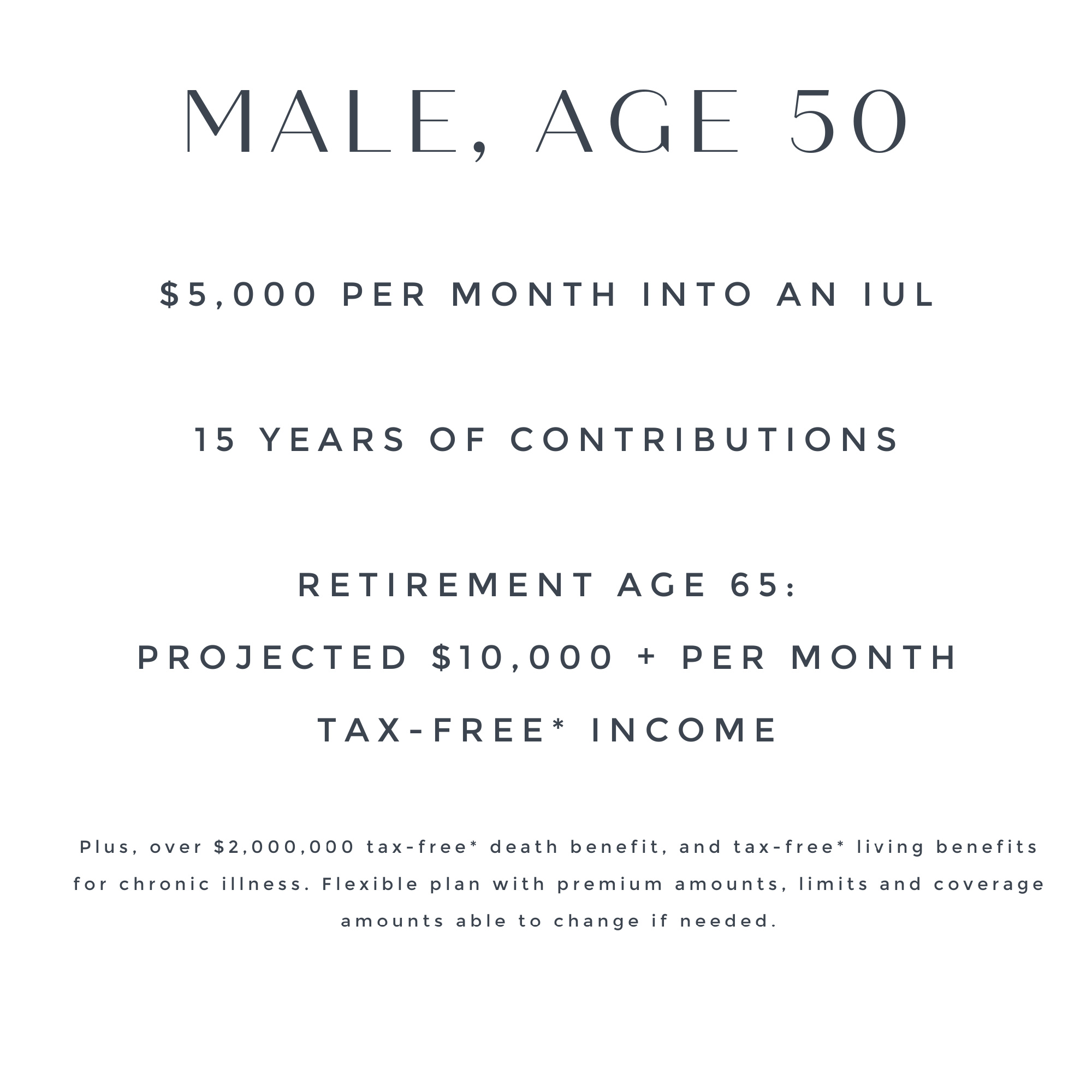

Mr. Johnson was a successful business owner, but had invested most of his money in his business rather than saving money for his retirement. At 50 years old, he realized that he needed to start planning for retirement, but was he too late? In working with his financial advisor, Mr. Johnson took into consideration several pre-tax and after-tax strategies, ultimately deciding that he would prefer to receive retirement distributions tax-free. Mr. Johnson chose a life insurance strategy that would offer him all of the tax efficiencies of a Roth IRA, with none of the limitations on income or contribution amounts.

Quantum’s Back-Office Support

At the request of our financial advisor partner, Quantum identified several cash value life insurance options for Mr. Johnson designed to offer him the best distribution potential for his retirement goal in 15 years. While working with our advisor partner on Mr. Johnson’s goals and objectives, we determined that $5,000 a month ($60K a year) was an ideal contribution amount for him to allocate to the life Insurance plan.

Life Solution

As Mr. Johnson’s retirement solution, he and his financial advisor utilized an IUL (indexed universal life)* insurance policy that was projected to distribute over $10,000 a month in 15 years after his contributions of $5,000 a month ($60K a year). Furthermore, this IUL solution also offered additional living benefits along with a death benefit if something happened to Mr. Johnson pre- or post-retirement.

Request a case design

It’s easy to find out how life insurance might work for your client, whether you are a current Quantum partner or considering a partnership. Call your Quantum Life Insurance Consultant at 800.440.1088 today!

*”Consumers love indexed universal life, a love affair that remained strong in the fourth quarter 2022, according to Wink’s Sales & Market Report”: https://insurancenewsnet.com/innarticle/indexed-universal-life-drives-strong-2022-sales-wink-reports

IUL policies are credited interest based on contract terms, but are not actually invested in the stock market; they are not subject to market risk like variable life policies. Life insurance guarantees are provided by life insurance carriers and are based on their financial strength and claims-paying ability. Terms are subject to each individual life insurance contract, and medical underwriting may be required. Life insurance policies are tax-free in most cases, but exceptions such as trusts named as beneficiaries may be subject to different tax rules.

A natural coach and leader with 20 years in the industry, Jim uses his vast experience to deliver the most successful strategies to our advisors.