November is long-term care awareness month. Here are five things you should know about LTC.

1. Statistics vary on how many people will need LTC.

With 10,000 people turning 65 every single day in America until around year 20301, there are varying statistics regarding the need for long-term care floating around out there—some as high as 75%.2 In late August, Morningstar put together their 2018 updated statistics, placing the percentage of people 65 or older who will need long-term care at 52%, the majority female.3

2. There are different types of facilities providing different levels of care.4

If you hear the words “long-term care” and automatically think “nursing home,” you should know that long-term care encompasses a wide range of options and a progression of choices. The most self-sufficient seniors might live in independent retirement living facilities, while assisted living often adds medication management, daily personal care, meals and housekeeping. Continuing care retirement communities (CCRCs) offer a tiered approach so that seniors can transition on site as they require more services. Adult foster care is available in private homes run by trained caregivers—there are even special homes designated for military veterans with chronic medical conditions overseen by the Dept. of Veterans Affairs.

Of course, nursing homes are also part of the spectrum, offering 24-hour supervision, nursing care, help with daily living activities and three meals per day. Secured memory care units, which are more expensive, are often located within nursing homes to provide a safe but more homey environment for people suffering with Alzheimer’s or dementia. Skilled nursing facilities (SNF) are not identical to nursing homes—they often staff doctors and nurses around the clock and offer physical rehabilitation services. People in these facilities may be bedridden, need two people move them, and require dialysis or other intensive treatments.

3. Long-term care costs are high, and rising.

According to Genworth’s 15th Annual Cost of Care Survey, the “blended annual median cost of long-term care support services has increased an average of 3% from 2017 to 2018, with some care categories exceeding two to three times the 2.1% U.S. inflation rate.” 5

Annual National Median Costs 2018 6

Homemaker Services: $48,048

Home Health Aide: $50,336

Adult Day Health Care: $18,720

Assisted Living Facility: $48,000

Semi-Private Room in a Nursing Home: $89,297

Private Room in a Nursing Home: $100,375

Most expensive states in order are Alaska, Hawaii, Massachusetts, New Jersey, Connecticut, New York, New Hampshire, North Dakota, Vermont, Delaware, Maine, Washington, Minnesota, Oregon and California.5

4. Alzheimer’s dementia is on the rise due to longevity.7

According to the Alzheimer’s Association, “Someone in the United States develops Alzheimer’s dementia every 66 seconds.” An estimated 5.5 million Americans—one in 10 people age 65 and older (10%)—are living with Alzheimer’s dementia, almost two-thirds of them women.

In addition to gender, race evidently also plays a role in the risk of developing the disease. Hispanics are about one and one-half times as likely to have Alzheimer’s or other dementia as whites, while African Americans are about twice as likely to have Alzheimer’s or other dementia as whites.

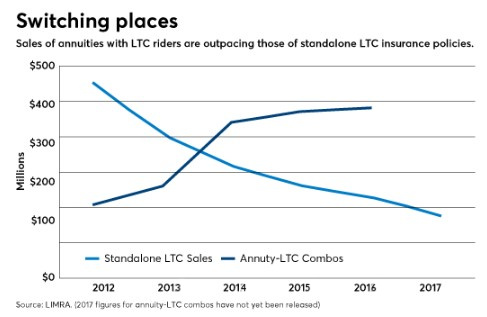

5. Hybrid policies are now more popular than standalone LTC policies.

When it comes to helping people solve the problem of potentially needing long-term care, hybrid whole life, hybrid indexed universal life (IUL) and hybrid annuities have been more popular than traditional long-term care policies, and they are becoming more popular every year.8

Demand for LTC coverage is actually on the rise, but dollars are flowing into other types of contracts. LIMRA reports that annuity-LTC hybrids surpassed individual LTC policies in sales for the first time in 2014.9

Demand for LTC coverage is actually on the rise, but dollars are flowing into other types of contracts. LIMRA reports that annuity-LTC hybrids surpassed individual LTC policies in sales for the first time in 2014.9

The reasons for the rise in popularity have to do with a combination of factors, including the rising cost of standalone LTC policies as well as the attractive features of some new hybrid annuities and life policies.

If you are a financial advisor and would like more information about hybrid policies, please call us at 800.440.1088. We can help you compare hundreds of products from more than 35 insurance carriers.

Sources:

1 “Baby Boomers Retire,” Pewresearch.org. https://www.pewresearch.org/fact-tank/2010/12/29/baby-boomers-retire/ (accessed November 5, 2018).

2 “Long Term Care Statistics,” LTCtree.com. https://www.ltctree.com/long-term-care-statistics/ (accessed November 5, 2018).

3 “75 Must-Know Statistics About Long-Term Care: 2018 Edition,” Morningstar.com. https://www.morningstar.com/articles/879494/75-mustknow-statistics-about-longterm-care-2018-ed.html (accessed November 5, 2018).

4 “What’s the Difference Between Types of Long-Term Care Facilities?,” USNews.com. https://health.usnews.com/wellness/aging-well/articles/2018-10-30/whats-the-difference-between-types-of-long-term-care-facilities (accessed November 5, 2018).

5 “Top 15 Most Expensive States for Long-Term Care: 2018,” Thinkadvisor.com. https://www.thinkadvisor.com/2018/10/24/top-15-most-expensive-states-for-long-term-care-20/ (accessed November 5, 2018).

6 “Cost of Care Survey 2018,” Genworth.com https://www.genworth.com/aging-and-you/finances/cost-of-care.html (accessed November 5, 2018).

7 “Alzheimer’s Is Accelerating Across the U.S.,” AARP.org https://www.aarp.org/health/conditions-treatments/info-2017/alzheimers-rates-rise-fd.html (accessed November 5, 2018).

8 “Why hybrid policies are so popular,” Thinkadvisor.com. https://www.thinkadvisor.com/2018/03/28/why-are-the-new-hybrid-ltc-policies-so-popular/ (accessed November 5, 2018).

9 “How clients can use annuities to pay for long-term care,” Financial-planning.com. https://www.financial-planning.com/news/as-ltc-insurance-prices-rise-long-term-care-annuities-gain-popularity (accessed November 5, 2018).

Further reading:

“Could Your Long-Term Care Premiums Be Hiding in Plain Sight?” Morningstar.com. https://www.morningstar.com/articles/879259/could-your-longterm-care-premiums-be-hiding-in-pla.html (accessed November 5, 2018).

“Hybrid policies for long-term care,” Chicagotribune.com. https://www.chicagotribune.com/business/sns-201806261243–tms–savingsgctnzy-a20180626-20180626-story.html (accessed November 5, 2018).

“Hybrid Policies Allow You to Have Your Long-Term Care Insurance Cake and Eat It, Too,” Elderlawanswers.com. https://www.elderlawanswers.com/hybrid-policies-allow-you-to-have-your-long-term-care-insurance-cake-and-eat-it-too-15541 (accessed November 5, 2018).