As a financial advisor, your clients expect you to know at least something about pretty much every subject that relates to money. For instance, a client might call you if they are thinking about refinancing or paying off their home, or even buying another car.

Holistic planners and financial advisors appreciate this, especially the ones that work with clients in the years leading up to and throughout retirement—the “decumulation” years. For instance, advisors who focus on comprehensive retirement planning have already figured out that helping people with federal benefits programs like Social Security is often necessary to optimize retirement income streams.

Social Security Help

Filing for benefits at age 62, when they first can, may result in a permanent reduction of as much as 30 percent of the benefits clients could have had had they waited. (Social Security benefits continue to increase by 8% per year up until age 70, which is a fairly hefty guaranteed return these days.)

Yet a recent survey by Nationwide shows that 45% of people mistakenly think that their benefits will go up automatically when they reached full retirement age, even if they file early.

That may be one reason that more than one-third don’t wait. According to the Center for Retirement Research, in the years leading up to the pandemic 31-34% of Americans filed for Social Security at age 62, while 30-36% waited and filed at their full retirement age.

Married couples, divorced people who were married for 10+ years, and widows/widowers have more filing options than simply waiting to file, and consumers want retirement advisors to help them plan the best filing strategy based on their health and circumstances.

According to the Nationwide research, 67% of U.S. adults would be interested in talking with a financial professional about creating income streams that would allow them to delay their Social Security filing, while 49% would be interested in discussing spousal benefit strategies for Social Security with a financial professional.

But another opportunity for retirement advice lies with Medicare.

How Medicare Can Fit into Your Practice

Planning for health care costs in retirement is a big deal. In fact, according to Fidelity, health care costs are often the largest expense that individuals and families face in retirement. Medicare can cost more than people expect, especially when premiums, deductibles and co-pays are factored in, so it’s important that your client’s retirement plan addresses future health care expenses and probable medical cost increases over time.

Fidelity estimates that an average retired couple age 65 in 2021 may need approximately $300,000 saved (after tax) to cover health care expenses in retirement, including Medicare premiums and out-of-pocket expenses.

Medicare Helps Some Advisors with Client Retention

Several of our advisors offer Medicare insurance, and they have told us that they have found that this makes their clients more loyal and less apt to switch advisors throughout retirement. Indeed, some of their clients call them annually the day Medicare Open Enrollment begins.

But even advisors who do not sell Medicare Advantage or Medigap insurance can use their knowledge and expertise to forge closer client relationships.

Remember, in most cases Medicare premiums get deducted out of Social Security checks each month, and higher-income clients pay more permanently with a five-year lookback period, which is an important consideration when helping them decide how and when to retire.

Medicare Versus Medicaid Confusion

In addition to thinking that Medicare is free starting at age 65, consumers may also think it covers long-term care. But Medicare does not cover stays in skilled nursing facilities which last longer than 100 days.

The similarity between the words Medicare and Medicaid may add to the confusion. Medicaid does cover long-term care (LTC), but only after the person who needs care is destitute or “spends down” everything until they have basically no assets left, which can financially harm spouses and heirs.

This is where retirement advisors can both educate and help clients.

According to the latest 2021 Genworth Cost of Care study, a private room in a nursing home costs almost $300/day, or nearly $9,000 per month. Quantum advisors have access to multiple hybrid LTC insurance policies and riders that can provide some funds for long-term care if it’s needed, or other benefit options like spousal income or death benefit to heirs if it isn’t. Long-term care insurance coverage for retirees is no longer “use it or lose it” because of these new hybrid product innovations.

Medicare Premium Increases

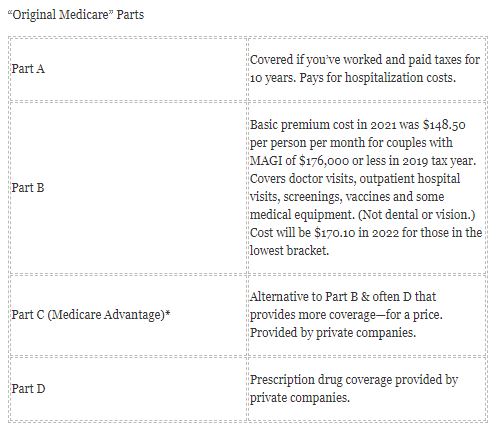

Due to the pandemic and expensive new treatments for Alzheimer’s, Medicare premiums just went up. On November 12, 2021, the federal government announced a 14.5% increase in Part B premiums. Those in the lowest income bracket will jump from $148.50 a month to $170.10 in 2022. Along with the premium spike, the annual deductible for Medicare Part B is rising to $233 in 2022, up from $203 in 2021.

Premiums are even higher for those with higher incomes. The additional amount of premium due is known as the income-related monthly adjustment amount, or IRMAA, and is based on tax returns with a five-year lookback. According to CNN, individuals earning $500,000 or more a year and joint filers making $750,000 or more annually will pay $578.30 a month per person for coverage in 2022.

Medicare Open Enrollment

Every year from October 15 – December 7 Medicare has an open enrollment period. Consider using this timeframe as another excuse to reach out to your clients nearing retirement or already retired in order to provide your financial expertise and strengthen your long-term relationship.

*Medigap plans are supplemental plans also sold by private companies which can cover additional costs as well as care outside the U.S.

With a degree in journalism and many years of experience, Pel creates content for websites, blog posts, social media, whitepapers, marketing pieces and more. She is passionate about SEO.