The Exclusion Amount Is Set to Drop January 1, 2026

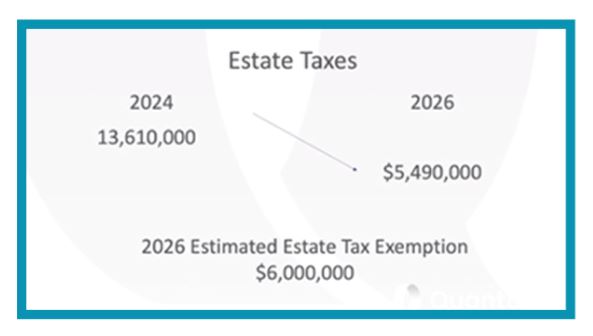

If you work with high-net worth clients, clients who live in areas with high home or real property values, or clients who own businesses, the time to plan for rising estate taxes is now. The exclusion for estate taxes today in 2024 is $13,610,000 per person (or $27,220,000 per couple) but without any changes to the current tax law, the exclusion will drop back down to its 2017 amount of $5,490,000 per person.

When adjusted for inflation, the 2026 estimated estate tax exemption will be around $6,000,000 per person, or $12,000,000 per couple:

Your clients want to provide for their families and leave as much to their heirs as possible. In 2018, thanks to the Tax Cuts and Jobs Act the estate tax threshold went from $5.49 million to over $11 million, making it easier to shield millions from taxes. Since the tax bill took effect, there are more billionaires than ever, worldwide numbering 540 in 2018 and jumping to 2,544 in 2024. Many of the wealthiest live in the United States.

Now, with the exclusion amount set to drop in 2026, you and your clients have less than two years to decide how their money will be transferred to the next generation. At Quantum, we have solutions!

Watch my video to learn more:

Below is a potential life strategy that may work for some clients. It may or may not be applicable to your client’s situation, and we recommend that you work in conjunction with your client’s tax professional as well as their tax and/or estate attorney before implementing any specific recommendations related to the client’s personal tax and estate situation. Additionally, the premium rates used in this example are estimates and may vary based on a person’s unique circumstances. Please contact us for a more accurate case design for your clients.

Case Study: 2026 Estate Tax Sunset Solution

Case Study: 2026 Estate Tax Sunset Solution

Hypothetical Dr. Jones Net Worth $50M

As stated, this year the estate tax exclusion amount is $13,610,000 per person—which will drop down to an estimated $6,000,000 for the 2026 tax year when adjusted for inflation. This will really affect hypothetical Dr. Jones, and he needs to do something about it as soon as possible.

Dr. Jones’ net worth is $50 million, which includes a variable universal life (VUL) policy with a $12 million death benefit. If he could move this death benefit outside of his estate, he could get his net worth down to $38 million.

– Back Office Support for Life Underwriting

Dr. Jones’ financial advisor turned to her life insurance distribution partner, Quantum, and our back-office support team quickly leapt into action. You see, Dr. Jones hadn’t seen a primary care physician in over five years, and he was a licensed pilot who owned a small plane. In other words, he might look risky to life insurance underwriters. Because of our inside industry knowledge and relationships, Quantum was able to do some pre-underwriting and found three insurance carriers willing to offer standard risk policies to Dr. Jones.

– Two-Part Proposed Solution

Quantum’s life insurance advanced planning team then began working with legal and tax professionals from our carrier partners to help determine the best way to transfer ownership out of an estate and into an appropriate trust. They looked closer at Dr. Jones’ variable universal life (VUL) policy which was personally owned by Jones and was not inside a trust. The VUL had $4 million in cash value and $12 million death benefit. They determined that the first step should be a 1035 exchange.

- 1035 Exchange of Variable Universal Life (VUL) Policy to an Indexed Universal Life (IUL) Policy

In conjunction with Dr. Jones’ CPA and attorneys, a 1035 Exchange was executed. A 1035 Exchange allows you to transfer funds from a life insurance policy to a new policy with better terms, without having to pay taxes. The new IUL policy gave Dr. Jones a $30 million death benefit, and replacing the policy also suppressed the cash value somewhat to slightly under $4 million. This was actually beneficial during the next step.

- Lifetime Gift Exemption Used to Gift the New Policy to an Irrevocable Life Insurance Trust (ILIT)

In addition to the sunset of the current high estate tax exclusion, the high lifetime gift tax exemption rate is also ending. For 2024, the lifetime gift tax exemption is $13.61 million, but this will be decreased beginning January 1, 2026 to $5 million, indexed for inflation. So, this year and next is the best window of time to utilize it.

Dr. Jones was advised by his CPA in conjunction with work done by Quantum’s advanced planning team to gift the new IUL policy into an ILIT trust utilizing his lifetime gift exemption. In Dr. Jone’s case, he used slightly under $4 million of the current $13.61 million gift exemption amount—or, the cash value of the new IUL policy. This leaves him with another $9.61 million remaining in the lifetime gift tax exemption amount to gift elsewhere in the next few months to further mitigate taxes.

The Resulting Benefits of The 1035 Exchange + ILIT Solution

- Quantum lowered Dr. Jones’ net worth, reducing the estate taxes he will owe.

- The advanced planning life team analyzed the situation, did some pre-underwriting, and worked closely with insurance carrier attorneys and Dr. Jones’ CPA, estate attorneys and financial advisor to create and help execute the 1035 Exchange + ILIT solution.

- The remaining lifetime gift amount of $9.61 million can be gifted in the next few months to further mitigate taxes.

It’s easy to find out how life insurance and/or trusts may help your client mitigate—and in some cases, even eliminate—your client’s estate tax problem. There are many solutions out there. Whether you are a current Quantum partner or considering a partnership with us, call me or your Quantum Life Insurance Consultant at 800.440.1088 today!

Nate has 15-plus years of life insurance distribution experience, and he is knowledgeable in both annuity and life insurance strategies. As part of the life team, he helps evaluate the ins and outs of hundreds of policies so they can recommend the best fit for an individual’s financial plan.