During a client’s accumulation phase, an investor can usually withstand and maneuver stock markets’ ebbs and flows. But at retirement, a new challenge begins as their planning resets. As clients retire with their pool of accumulated retirement assets, the distribution phase starts, and the biggest obstacle to success often depends on how the markets perform. If clients happen to retire in a stable or up market, they can usually retire successfully even with limited planning. However, if clients retire in a down market, without proper planning and the help of

a financial advisor they can face multiple issues, including sequence of returns risk during the early years of retirement which can erode retirement savings and potentially force a retiree back into the workforce.

Other risks to retirement include:

Quantum has frequently discussed the four phases of an investor’s lifecycle, the critical protection and distribution phases for investors planning for retirement, and how annuities can help mitigate certain risks in retirement.

But another tactic that should be given serious consideration is the introduction of permanent life insurance to the financial plan during the accumulation phase of the investor’s lifecycle.

Let’s examine how permanent life insurance with a focus on cash value should be used as an asset class during the accumulation phase to help mitigate risk in retirement.

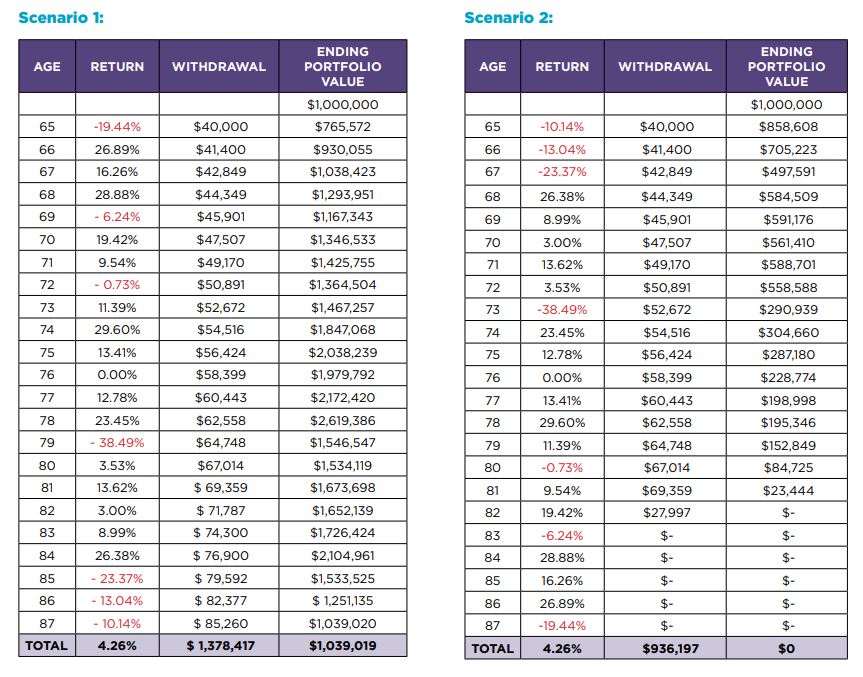

Sequence of Returns Risk Is All About Timing

Two Scenarios with Exactly the Same Returns—In Reverse Order

• In both scenarios, the retiree is 65 years old and retires with $1 million.

• In both scenarios, the retiree withdraws 4% per year plus a 3.5% annual increase for inflation each year through age 87.

• Scenario 2 shows the actual S&P 500 Index stock market returns from the years 2000 thru 2022. Scenario 1 simply inverts and reverses those same returns, starting with the 2022 S&P 500 Index return.

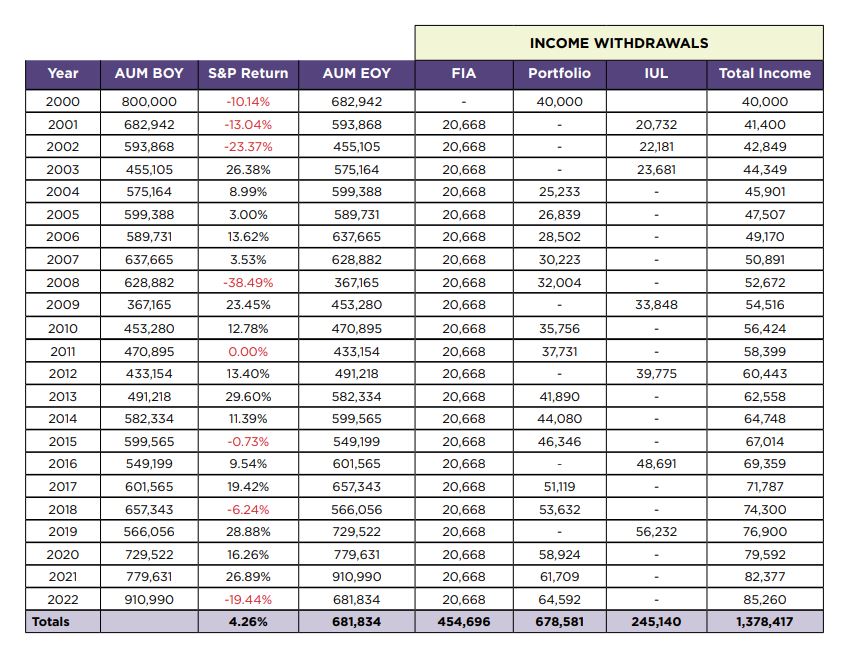

Introducing Permanent Life Insurance and a Fixed Indexed Annuity Into the Plan

Planning

• Client is 40 years old.

• $1,000 premium per month for 20 years.

• At age 60, move $200,000 from AUM to a fixed indexed annuity (FIA) with guaranteed income rider.

• Retire at age 65.

• 4% withdrawal rate starting in retirement.

• 3.5% annual inflation adjustment.

• After first year of negative returns, trigger the FIA lifetime income.

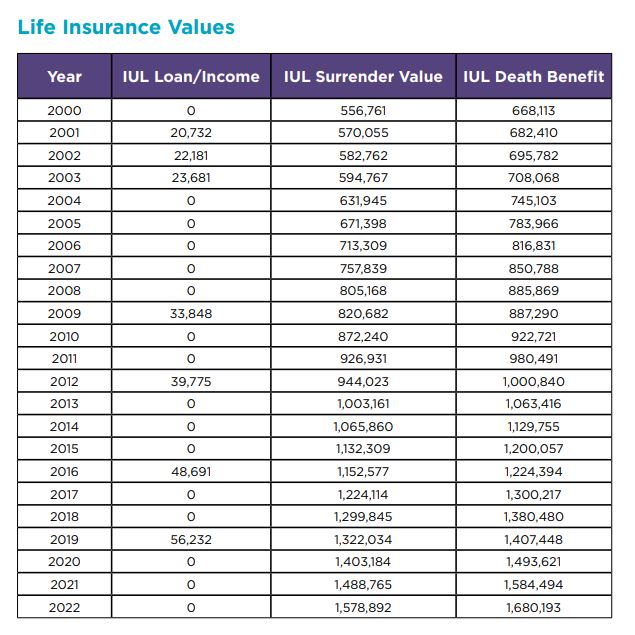

• After each year the AUM portfolio has negative returns, take the AUM income from the IUL policy in the

form of a loan.

– This keeps more money in the investment portfolio and exposed to market returns.

– Permanent life insurance loans have special tax treatment.

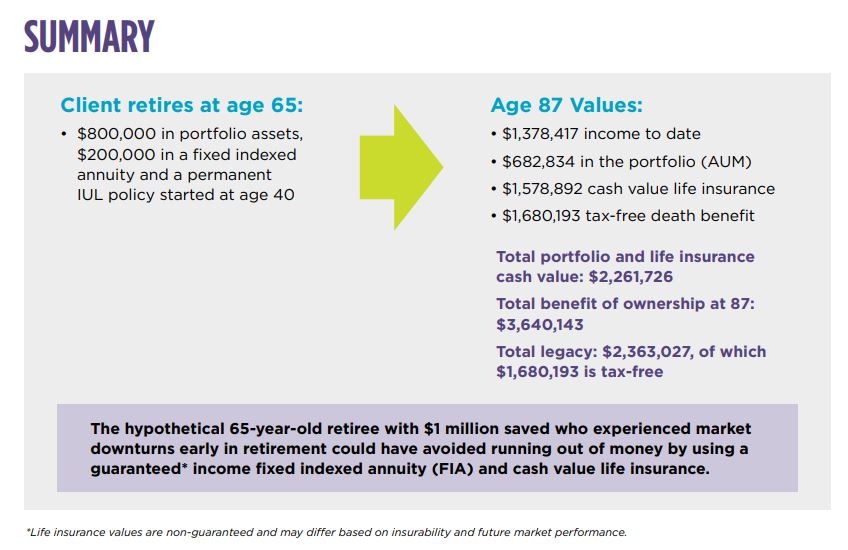

If the client had allocated $200,000 of the portfolio into a fixed indexed annuity with guaranteed income at age 60 during the protection phase of the client’s investor life cycle before retirement, the FIA could generate $20,668 in guaranteed income annually and $454,696 in total as shown, assuming income is deferred to age 66, the year after his portfolio suffers a negative return.

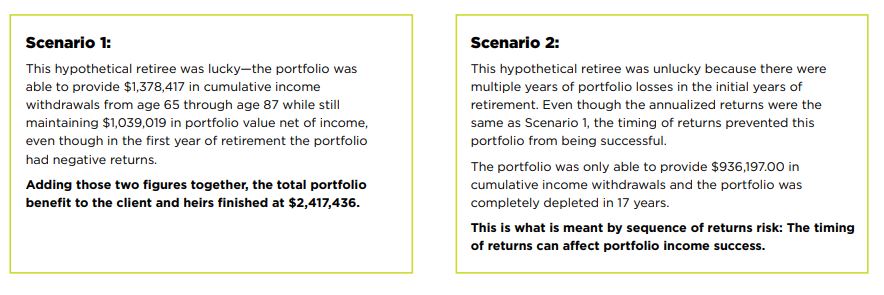

By accessing cash from the permanent life insurance policy following down years to supplement income in retirement, the client can avoid selling into market losses. In effect, the client can preserve his traditional retirement funds instead of selling at potential market bottoms, giving those assets time to recover. In this scenario, not only did the client not exhaust his life savings, but he has taken $1,378,417 in total income, has $2,261,726 in liquid assets, and a legacy of $2,363,027 at age 87.

Adding permanent life insurance and guaranteed income from a fixed indexed annuity to the mix of asset classes serves an important role in the holistic financial plan, especially when it comes to mitigating risk in retirement. The combination of traditional asset classes, fixed indexed annuities with lifetime income, and permanent life insurance can dramatically improve a client’s retirement and tax-advantaged legacy passed on to their loved ones.

A fixed indexed annuity (FIA) with an optional guaranteed income rider* provides guaranteed lifetime income that may help offset portfolio sequence of returns risk. Guaranteed income lessens the reliance on the portfolio to generate income, helping mitigate the risk of negative timing of returns and providing security to cover income needs.

Having guaranteed income gives the retiree the option to leave money in the portfolio during market downturns rather than being forced to take withdrawals for living expenses which can hasten a portfolio’s decline.

*Guaranteed by an insurance carrier. Optional enhancement riders may be added to the policy for an additional charge. These are hypothetical average numbers based off rates obtained from A+ rated carriers.

This material is not a recommendation to buy, sell, hold, or roll over any asset, adopt a financial strategy or use a particular account type. It does not take into account the specific investment objectives, tax and financial condition or particular needs of any specific person. You should work with tax, legal and financial professionals to discuss your specific situation.

Indexed universal life (IUL) insurance policies are not stock market investments, do not directly participate in any stock or equity investments, and do not receive dividend or capital gains participation. The past performance of an index is no indication of future crediting rates. Loans and death benefit payments from indexed universal life policies have special tax treatment and could be tax-free.

A natural coach and leader with 20 years in the industry, Jim uses his vast experience to deliver the most successful strategies to our advisors.