Tim and Ann’s Legacy Goal

Tim, age 38, and Ann, age 37, are healthy young nonsmokers with three little children. Tim is a very high-earning attorney, and he and Ann want to maximize a tax-advantaged legacy for their children. They plan to create an irrevocable trust to accomplish their legacy goals. The “irrevocable” part means parents can’t touch any cash value they place into the trust—assets are strictly for wealth transfer to the beneficiaries.

1. The Insurance Solution

Life Insurance Solution Inside ILIT (Irrevocable Life Insurance Trust)

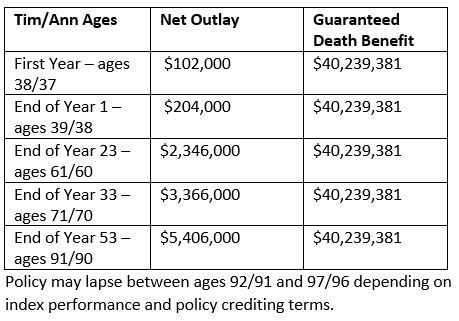

Policy: Survivorship IUL (Indexed Universal Life). The policy’s death benefit for the three children pays into the trust when the second policyholder dies.

Cost: $102,000 each year for 59 years. The cost of the insurance was decided based on current gift tax limits. For 2023, each spouse can gift $17,000 per year to each child tax-free; therefore, $17,000 x 2 x 3 children = $102,000.

Death Benefit Amount: The death benefit amount that will pay into the irrevocable trust for the children when both parents have passed away is more than 40 million dollars.

With IUL, there is the chance for growth in the policy depending on the chosen index’s stock market performance. The numbers shown below are from a real case design run in September of 2023, but your case design or illustration may vary depending on multiple factors.

Actual payouts may be higher than those shown here based on index results; these are the minimum guaranteed amounts outlined in the policy. Guarantees are backed by the financial strength of the issuing carrier.

This particular Survivorship IUL policy was designed to pay a large death benefit during the time when Tim and Ann’s children would most need protection and legacy. As the policy continues through time, its cash value is designed to grow up to parents’ ages 61/60, then in subsequent years, utilize cash value to pay additional costs of insurance as the policyholders become more likely to pass away. If parents live past their life expectancy in their 90s, the policy lapses. By this time, it is expected that their beneficiaries, if still living, have other resources.

2. The Investing Solution Comparison

Investing the premium amount in the stock market

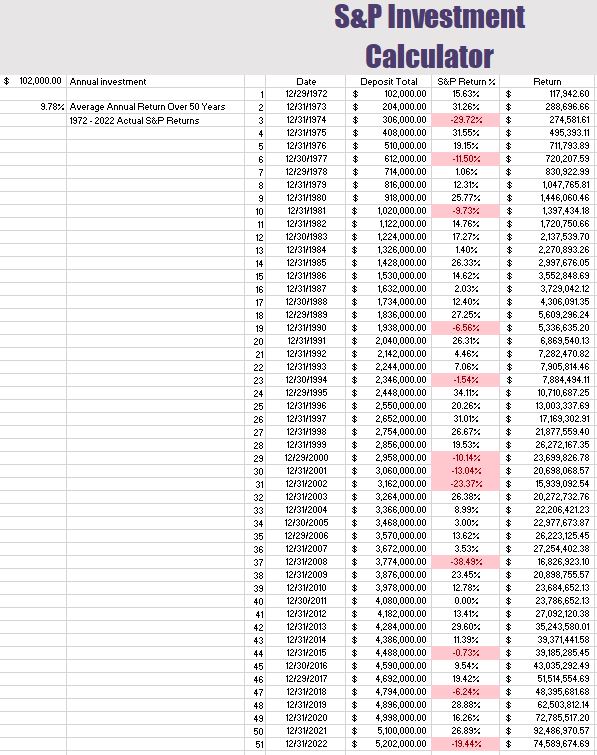

So, what if your client says that he or she could take that $102,000 per year and invest it in the stock market instead, also inside an irrevocable trust? Taxes are not considered in this comparison; this is a simplified example. If a large legacy for the children is the goal, you can see from the chart below how long it will take to build up the desired amount if funds are placed in the stock market.

The example below shows actual average S&P stock market returns from 1972 to 2022, and what would have happened if Tim and Ann had invested $102,000 per year and earned those total actual average returns rather than paying the $102,000 per year premium for a Survivorship IUL policy.

As you can see, it could take 44 years of investing to have $40 million. What if your clients die sooner?

* Life insurance policies are tax-free in most cases, but exceptions such as trusts named as beneficiaries may be subject to different tax rules. Surrender charges may apply if the clients no longer want the IUL policy for some reason during the first years of ownership—the surrender charges timeframe will be specified in the policy contract.

Consumers love indexed life, sales were up 28% in the second quarter of 2023, according to Wink’s Sales & Market Report: https://insurancenewsnet.com/innarticle/indexed-life-sales-up-28-drives-strong-q2-for-life-insurance-wink-says

IUL policies are credited interest based on contract terms but are not actually invested in the stock market; they are not subject to market risk like variable life policies. Life insurance guarantees are provided by life insurance carriers and are based on their financial strength and claims-paying ability. Terms are subject to each individual life insurance contract, and medical underwriting may be required.

Request a Case Design!

It’s easy to find out how life insurance might work for your actual client, whether you are a current Quantum partner or considering a partnership. Call your Quantum Life Insurance Consultant at 800.440.1088 today!

Paul Payne spearheads our life insurance training program at Quantum, called QVida. With more than two decades spent in the life insurance and wealth planning industry, Paul has gathered a treasure trove of educational material developed by experienced professionals, including attorneys, CPAs, tax professionals, authors, financial experts and pension, employee benefit and retirement experts which he incorporates into his seminars and workshops. Learn More