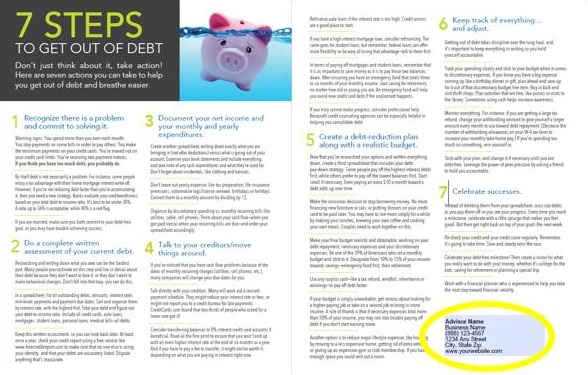

As part of our ongoing support of our financial advisor partners, we continue to develop a deeper pool of original content and resources designed to help advisors with their consumer client education. Recently we finished “7 Steps to Get Out of Debt”, available as a customizable PDF (front and back, 8-1/2″x11″).

Call us at 800.440.1088 to learn more about how we create customized materials like these for you to share with your clients.

The “7 Steps to Get out of Debt” whitepaper includes detailed instructions about how your clients (or their children) can go about getting themselves above water in terms of their finances. The seven steps include:

- Recognizing there is a problem and committing to solving it.

- Doing a complete written assessment of current debt.

- Documenting net income and monthly and yearly expenditures.

- Talking to creditors / transferring / refinancing / asking for lower rates.

- Creating a debt-reduction plan in conjunction with a realistic budget.

- Keeping track of everything and making adjustments.

- Celebrating successes.

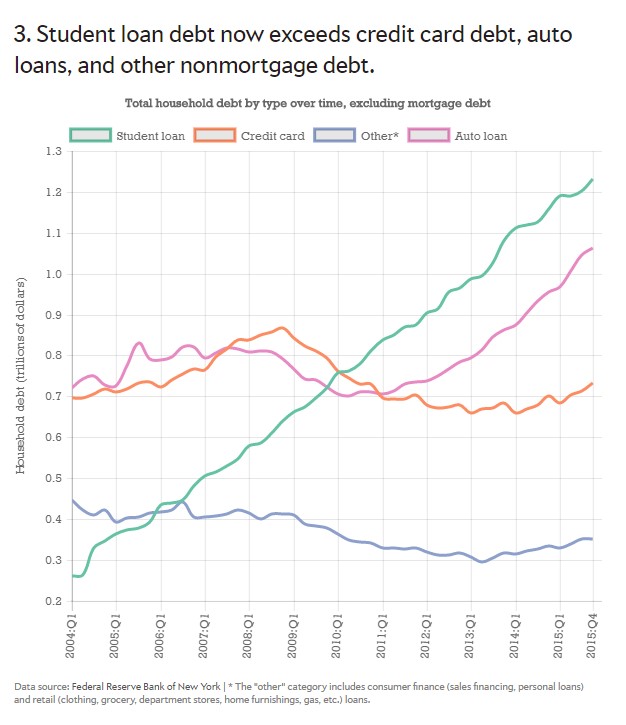

As we were working on the whitepaper, we wanted to know just how big the problem of consumer debt was in America. The statistics are pretty sobering.

According to an article published in Slate on May 12, 2016: “Five Charts That Show Americans Families’ Debt Crisis”, U.S. households owe trillions in student loans, credit card loans, auto loans, and mortgages. Below is chart #3 which highlights one of the biggest changes in American debt since 2004—student loan debt—which now exceeds credit card, auto and other non-mortgage debt. Crushing student loan debt not only affects young college graduates, but also affects their parents—who find themselves unable to fund their own retirements due to the student loan repayment burden.

Thirty-seven percent of U.S. parents say their children’s college education is more important than their own retirement savings, according to a survey by HSBC Group. Sixty percent of U.S. parents would go into debt to fund their child’s college education, and 58% say that, while the expense makes it more difficult to keep up with other financial commitments, it is more important.

This presents a unique opportunity for the financial advisor who can offer solutions to college funding. If you are a financial advisor, contact us to learn more about college funding options.

Other information and links:

The number one financial stressor for both men and women is paying off debt.