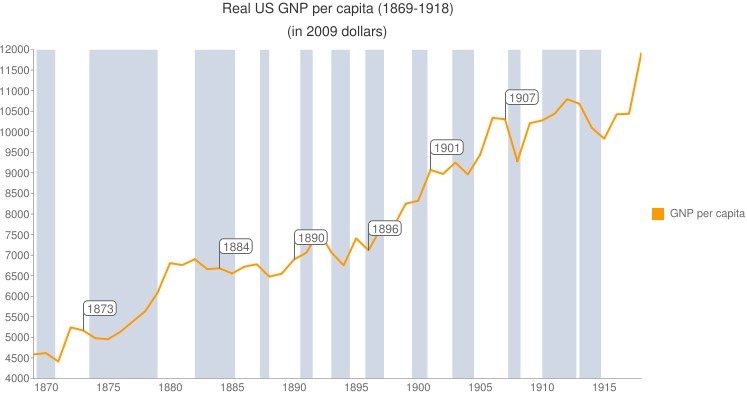

The shift from our rural, agrarian economy to a full-fledged Industrial Revolution began in the mid-1800s and was accelerating rapidly by the turn of the 20th century in the United States.

Source: Wikipedia

In the beginning of our nation’s history, homesteaders or farmers might make money or barter when they produced more than they consumed. Retirement wasn’t an option…or even a concept. Most people worked the land their entire lives and had large families with lots of children to help out.

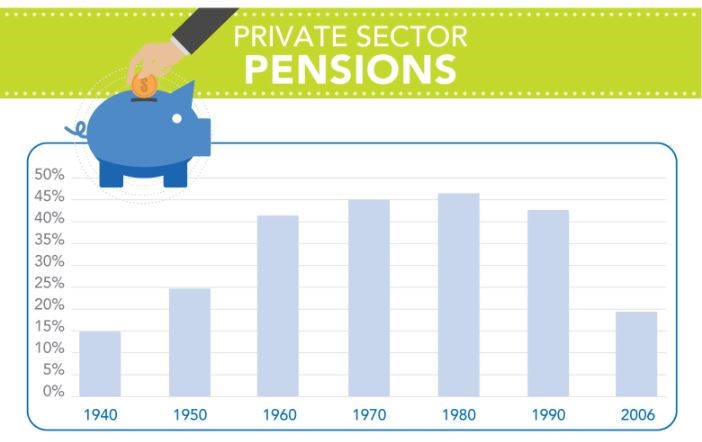

With increasing populations flocking to cities to work for companies and factories—usually for one company their entire life—compensation and retirement became concerns. The pension was born in 1875 when the American Express Company established the first private pension plan in the U.S. in an effort to create a stable, career-oriented workforce.

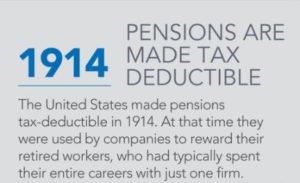

Pensions were usually paid, for life, in regular installments after retirement, and were often based on length of service and former salary. Today’s pensions—the few that remain—are usually paid monthly, although some retirees may be offered the choice of a lump-sum payment. In 1913, the U.S. introduced income taxes, and the Internal Revenue Service ruled in 1914 that pensions paid to retired employees were tax-deductible for private companies because they were similar to wages as necessary business expenses.

Pensions continued to be offered by more companies until around 1980, when they began to decline as companies introduced defined benefit plans, such as the 401(k).

A recent article in Bloomberg spelled out some of the issues retirees have been facing since the decline of the pension:

“Company after company has repudiated traditional pensions, pushing younger workers into 401(k)-style retirement plans. For diligent savers, a 401(k) can accumulate a big balance, but when the time comes to start using it, things will get a lot more complicated than it was for their parents.”

“Retiring workers have no idea how markets will perform during the rest of their lives. They also don’t know how long they’ll live. A healthy 65-year-old man now has a 25 percent chance of dying by age 78, but he has the same chance of living to 91 or beyond, according to the Center for Retirement Research. Longevity is increasing, and retirees could end up living far longer than they expect. With a pension, you were paid until you died. With a 401(k), you could come up short.”

We provide financial advisors access to hundreds of retirement solutions from multiple insurance carriers. In fact, fixed indexed annuities (FIAs) can be likened to pensions because they can offer monthly income for life, depending on the policy terms. To discuss a full range of strategies to help your clients, contact Quantum at 800-440-1088.

See complete infographic here.