Below is a potential life strategy that may work for some clients. It may or may not be applicable to your client’s situation, and we recommend that you work in conjunction with your client’s tax professional as well as their tax and/or estate attorney before implementing any specific recommendations related to the client’s personal tax and estate situation. Additionally, the premium rates used in this example are estimates and may vary based on a person’s unique circumstances. Please contact us for a more accurate case design for your clients.

John and Jane’s Legacy Goal

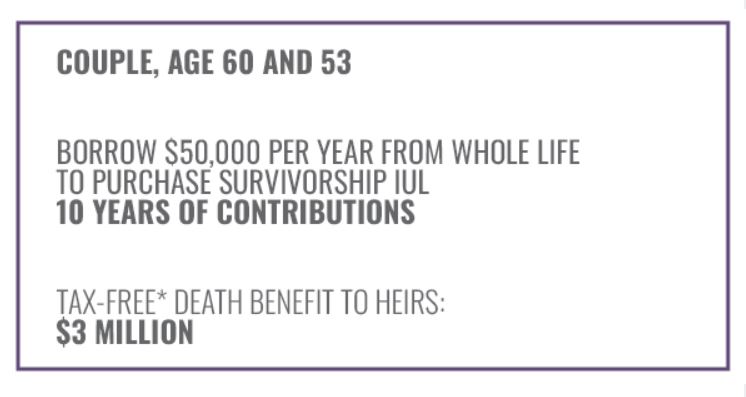

As John, age 60, and Jane, age 53, discussed their financial situation and retirement goals with their financial advisor, they soon revealed their biggest desire: To leave more wealth to their children and grandchildren. In looking at their cash flow as well as all of their available resources, John and Jane’s financial advisor found a way for them to leverage the cash value in an existing whole life policy that they then used to buy a survivorship indexed universal life policy.

The result? An additional $3 million tax-free death benefit for their heirs.*

Life Solution: Borrowing from Whole Life to Fund Survivorship IUL

A survivorship IUL policy is permanent life insurance on two people which pays a death benefit when the second insured passes away. After reviewing their options with their advisor, John and Jane decide to borrow from John’s whole life policy to leverage its cash value to purchase a survivorship IUL policy that would pay a high tax-free* death benefit to their children and grandchildren.

Here’s how it works.

Existing policy: The death benefit on John’s existing whole life policy is $1 million with Jane named as the beneficiary and their children and grandchildren named as secondary beneficiaries. The cash value in the whole life policy is $500,000, which they can borrow from at an interest rate of 6%.

New policy: John and Jane’s new survivorship IUL policy with a death benefit for their heirs of $3 million would cost approximately $50,000 per year for 10 years based on their health and ages.

John and Jane decide to borrow the $50,000 per year needed for 10 years and pay roughly only $3,000 in interest per year on each $50,000 borrowed. Per their policy terms, they could actually pay this back, or let the cash value in the policy pay the interest as long as they didn’t let their policy lapse.

The attached illustration, which is an actual illustration from Nationwide®, shows all of the contract terms and details.

Download Nationwide Illustration

Request a case design

It’s easy to find out how life insurance might work for your client, whether you are a current Quantum partner or considering a partnership. Call your Quantum Life Insurance Consultant at 800.440.1088 today!

* Life insurance policies are tax-free in most cases, but exceptions such as trusts named as beneficiaries may be subject to different tax rules. Surrender charges apply if the clients no longer want the IUL policy for some reason during the first 15 years of ownership. In a worst-case scenario, the new IUL policy may lapse at some point in the future without additional premiums paid depending on performance. Conversely, based on historic return data, the IUL policy may grow in value over and above the $3 million death benefit depending on the actual annual interest which is credited to the new IUL policy. See the illustration for more details.

”Consumers love indexed universal life, a love affair that remained strong in the fourth quarter 2022, according to Wink’s Sales & Market Report”: https://insurancenewsnet.com/innarticle/indexed-universal-life-drives-strong-2022-sales-wink-reports

IUL policies are credited interest based on contract terms but are not actually invested in the stock market; they are not subject to market risk like variable life policies. Life insurance guarantees are provided by life insurance carriers and are based on their financial strength and claims-paying ability. Terms are subject to each individual life insurance contract, and medical underwriting may be required.

A natural coach and leader with 20 years in the industry, Jim uses his vast experience to deliver the most successful strategies to our advisors.