Meet Bob Business Owner, Age 35

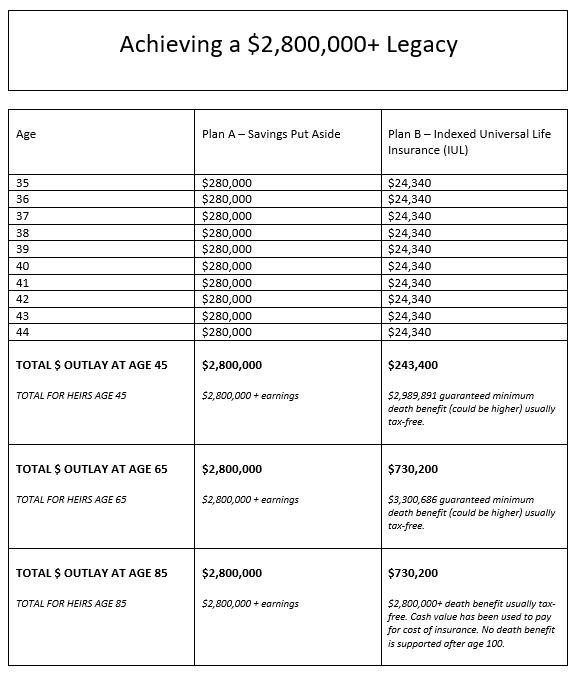

Bob’s business is doing great, he is healthy, and he feels he can save up enough money to leave his family in good shape when he dies. Calculating the total of all of the desired legacy amounts that he’d like to leave to each family member, he and his financial advisor estimate that he will need around $2.8 million at his passing.

The question is: Is it better and more economical for him to save and put aside this amount, or should he purchase a life insurance policy?

A Look at the Numbers

For this example, we looked at how much Bob would need to put aside or invest every year versus pay in insurance premiums.

Plan A shows how much money Bob will need to save/invest/set aside in order to achieve his legacy goal. Using an IUL for Plan B above, Bob’s death benefit can grow over time through cash accumulation and crediting based on the growth of a benchmark index, such as the S&P 500. Full details are in the attached downloadable illustration below.

How This Works

How This Works

It is important to recognize that this example is created simply to compare legacy and inherited amounts if the business owner does not touch funds. The use of pretax or after-tax funds for Plan A savings are not considered. Neither are rates of return for Plan A, nor its liquidity in comparison to the cash value in an IUL policy. Potential market losses for Plan A are also not considered.

With IUL used for Plan B above, Bob’s death benefit can grow over time up to age 65 through cash accumulation and crediting based on the growth of a benchmark index, such as the S&P 500. The death benefit amounts shown above are based on guaranteed minimums, but could be higher depending on index performance. The policy is designed to be fully paid at age 65. After age 65, cash values are designed to be used to pay for insurance so death benefit amounts start to go back down through time.

This downloadable sample illustration from North American®—for a 35-year-old healthy male “John Doe,” not an actual individual—shows all of the contract terms and details. Please call the life insurance consultants at 800.440.1088 to receive an actual personalized illustration for your client, where terms and premiums may vary.

Download the IUL Illustration

Life Insurance Advantages for the Business Owner

1) Cash Outlay

Putting away $24,340 per year for 30 years is a lot more realistic for Bob than putting away $280,000 a year for 10 years. Life insurance companies are in the insurance/death benefit/legacy business, Bob shouldn’t be. For this scenario, the total cash outlay for Bob for Plan A is $2,800,000. Total cash outlay for Bob for Plan B life insurance is $730,000, with premiums fully paid at age 65*.

Additionally, it’s important to recognize that should Bob pass away unexpectedly, his legacy will be assured from the very first day the policy is in force and up to age 100 using insurance as long as his premiums are paid.

2) Taxes to Bob

The earnings or gains on Plan A savings could be taxable to Bob, while account value credits to the Plan B indexed universal life insurance policy are not.

3) Taxes to Heirs/Probate

Plan A savings could be taxable to heirs. And if there is no estate plan or the estate is contested, Plan A savings could end up in probate court, with additional fees, long court timeframes, and headaches for heirs. In almost all cases, with Plan B life insurance left to individual beneficiaries, the death benefit amounts are tax-free and bypass probate.

4) Market Risk

If Plan A savings are invested in the stock market, they will be subject to market risk. But indexed universal life is not. Even though IUL crediting is based on the performance of a stock market index, IUL is a contract with guarantees provided by the financial strength of the insurance company. If the stock market shows a loss, the credit for the IUL policy can’t go lower than 0%. This is different than variable life policies, which can lose value during down markets. NOTE: Although the IUL policy isn’t subject to stock market risk, there may be surrender fees if the policy does not stay in force as long as initially planned.

*Life insurance policies are tax-free in most cases, but exceptions such as trusts named as beneficiaries may be subject to different tax rules. Surrender charges apply if the client no longer wants the IUL policy for some reason during the first 15 years of ownership. In a worst-case scenario, the new IUL policy may lapse at some point in the future without additional premiums paid depending on performance. Conversely, based on historic return data, the IUL policy may grow in value over and above the $2.8 million+ death benefit depending on the actual annual interest which is credited to the new IUL policy. See the illustration for more details.

”Consumers love indexed universal life, a love affair that remained strong in the fourth quarter 2022, according to Wink’s Sales & Market Report”: https://insurancenewsnet.com/innarticle/indexed-universal-life-drives-strong-2022-sales-wink-reports

IUL policies are credited interest based on contract terms but are not actually invested in the stock market; they are not subject to market risk like variable life policies. Life insurance guarantees are provided by life insurance carriers and are based on their financial strength and claims-paying ability. Terms are subject to each individual life insurance contract, and medical underwriting may be required.

Request a case design for your client!

It’s easy to find out how life insurance might work for your client, whether you are a current Quantum partner or considering a partnership with us. Call your Quantum Life Insurance Consultant at 800.440.1088 today!

A natural coach and leader with 20 years in the industry, Jim uses his vast experience to deliver the most successful strategies to our advisors.